If you’re in a LLC dispute, read your operating agreement carefully!

Continue readingWrongful Eviction in Georgia

[We apologize, but our office no longer accepts tenant wrongful eviction claims. If you are a tenant, please contact Georgia Legal Aid at www.georgialegalaid.org or the Atlanta Volunteer Lawyers Foundation at https://avlf.org/get-help/evictions/.]

There is a lot of confusion regarding evicting a tenant and wrongful eviction. One question is the amount of damages a tenant is entitled to if wrongly evicted. The issue was addressed recently by the Georgia Court of Appeals in Hart v. Walker, 347 Ga. App. 582 (2018). In that case, the landlord wrongfully evicted the tenant by changing the locks when she and the tenant got into a dispute.

If you’re a landlord, please don’t do this—in almost all instances, a landlord in Georgia must file an eviction in court to deprive a tenant of possession. Georgia is not a self-help state.

In the Hart case, the tenant sued the landlord claiming wrongful eviction and damage to personal property. He also claimed out-of-pocket expenses. The trial court ruled that although the tenant was wrongfully evicted, the tenant wasn’t entitled to recover damages against the landlord. The appeals court agreed. At trial, the tenant’s expert testified to the fair market value of the items, but the tenant couldn’t convince the trial court that he owned the items in question. The appeals court explained that the trial court could consider the credibility of a witness and, if the witness isn’t credible, can reject the witness’ testimony. Here, the trial court didn’t believe the tenant that he owned the items in question. Regarding the tenant’s out-of-pocket expenses for food and a motel, the appeal court noted that the tenant would have to incur such expenses regardless of the wrongful eviction. Therefore, these damages were too remote.

While this case addressed damages, as a landlord, if there’s a takeaway from this blog, it is that changing the locks wrongfully evicting a tenant isn’t the way to go. The landlord, in this case, was fortunate that the tenant could not recover significant damages.

Tax Deed Titles in Georgia

If you’ve purchased a tax deed in Georgia, how do you obtain a clear tax deed title, i.e., marketable title? That’s a question we get frequently. First and foremost, following a tax sale, you need to bar the right of redemption of the owner who didn’t pay taxes and any party who holds an interest in the property. We have covered this topic in other blogs on this website. But what about after you’ve barred the right to redeem? Are you able to put up a for sale sign and sell the property?

Generally, the answer is no if there’s a non-judicial tax sale on the property within the past 20 years. In other words, most title insurance companies won’t title insure such properties. So what do you do? There are generally three ways to obtain full title or what is known as “marketable title.”

The first way is to adversely possess the property for more than four years. Adversely possessing means taking full possession of the property in a manner that is (i) hostile (against the right of the true owner and without permission); (ii) actual (exercising control over the property); (iii) exclusive; (iv) open and notorious (using the property as the real owner would, without hiding occupancy); and (v) continuous.

The second way is to get a quitclaim deed from the owner who didn’t pay taxes and any party with an interest in the property.

The third way is to file a quiet title action in the Superior Court where the property is located. In such a lawsuit, the owner who didn’t pay taxes and any party with an interest in the property are named and allowed to object. A special master is appointed and ultimately the cour will issue an order clearing title. The order is recorded on the public record and the process is complete.

Please call us with any questions regarding tax deeds or the above methods of obtaining marketable title.

Discovery From Third-Parties

Once a lawsuit is filed, there is a period of discovery in which the parties exchange evidence and take depositions. In almost every case, there is tension in regard to what must be disclosed to the other side. Georgia law says that parties may obtain discovery regarding any matter, not privileged, which is relevant to the subject matter involved in the pending action, whether it relates to the claim or defense of the party seeking discovery. It is not grounds for objection that the information sought will be inadmissible at the trial if the information sought appears reasonably calculated to lead to the discovery of admissible evidence.

What does this mean? Well, it means that most anything that is or may become an issue in the litigation must be disclosed. The same rationale applies to discovery to a third-party (i.e., a party that is not named in the lawsuit). The way this is applied, as a practical matter, is that the court will look at issue in dispute and decide whether the information or documents sought are relevant or likely to lead to the discovery of admissible evidence. This is a liberal standard but there must be some connection between the evidence sought and a dispute in the lawsuit.

Service by Publication in a Quiet Title or Tax Deed Barment

In both a tax deed barment and the subsequent quiet title, a critical part of the procedure is serving all parties with an interest in the subject property. This includes lien holders, heirs, and anyone else with a claim against the property.

Often in these situations, especially when the property is distressed or abandoned, parties connected with the property may be hard to find. The best example is the delinquent taxpayer. That party has not paid taxes for one or more years, and, many times, has abandoned possession. If the delinquent taxpayer is gone and hasn’t left a forwarding address, that party may be anywhere.

What must be done in these situations? A reasonable and diligent search must be conducted to find and serve each party that has an interest. In a barment, this requires personal service for parties residing in the county of the tax sale or certified mail for parties residing outside the county. In a quiet title, personal service is required.

What if personal service or certified mail is unsuccessful? For example, you get back the certified letter stating it is undeliverable. In those situations, you’re entitled to serve by publication. This usually means advertising notice of the barment or lawsuit in the official county newspaper for four consecutive weeks.

Sound simple . . . usually it is straightforward, but there are times when things don’t work out as expected. In a recent case, Dukes v. Munoz et al., A18A0572 (decided June 15, 2018), a tax deed holder, unable to serve the delinquent taxpayer, hired an investigator. The investigator came back saying the delinquent taxpayer could not be found after reasonable search. Relying on the investigator’s testimony, the tax deed holder barred the taxpayer’s right of redemption and filed a successful quiet title action.

Happy tax deed holder and end of story . . . not so much. Turns out that the delinquent taxpayer was a Georgia state legislator, who found out about the barment and quiet title. The Georgia Court of Appeals ruled that because a Google search would have provided the address for the delinquent taxpayer, the tax deed holder had not exercised proper diligence in locating the delinquent taxpayer. Therefore, service by publication was improper and the barment and quiet title were voided; the tax deed holder was forced to incur the expense of the barment and quiet title.

The takeaway is that it’s not sufficient to use the last known address of party if that address appears invalid. The best approach, in our opinion, is to spend a little extra money to make sure parties with an interest are served and given a proper opportunity to object.

Excess Tax Sale Funds in Georgia

Following up on a previous blog regarding whether redeeming parties get priority to claim excess tax sale funds (they don’t), this blog discusses the process of disbursing excess funds following a tax sale.

Under Georgia law, a tax commissioner holds excess funds generated by a tax sale in a fiduciary capacity. Alexander Investment Group v. Jarvis, 263 Ga. 489, 491-492 (1993). Georgia statutory law, in O.C.G.A. § 48-4-5, describes the process of disbursing excess tax sale funds.

If there are any excess funds after paying taxes, costs, and all expenses, within 30 days of the tax sale, written notice is sent by first-class U.S. Mail to the following parties: (1) the owner of the property (delinquent taxpayer), (2) security deed holder, and (3) parties with a properly recorded interest in the property.

The notice of excess tax funds shall describe the land sold, the date sold, the name and address of the tax sale purchaser, the total sale price, and the amount of excess funds. The notice shall also state that the excess funds are available for distribution to the owner or interest holders in the order of priority in which their interests exist on the public record.

If excess funds are unclaimed or a dispute arises regarding who’s entitled to the excess funds, the tax commissioner or sheriff is entitled to deposit the funds into the registry of the superior court so that the superior court can disburse the funds.

If the excess funds remain unclaimed for five years, the funds may be retained. After this time, only a court order from an interpleader action filed in the county where the tax sale occurred, by the claimant for the funds, shall serve as justification for release of the funds.

Langley: Important New Personal Injury Case

Langley v. MP Spring Lake, LLC, A18A0193 (May 1, 2018), just issued by the Georgia Court of Appeals, may have a big impact on many future Georgia personal injury cases. Langley involves a residential landlord-tenant relationship in which a tenant sued her landlord for injuries more than a year after the injuries occurred. Normally, in Georgia, an injured party has two years to file a personal injury lawsuit. However, in this case, the landlord moved to dismiss the case because the lease provided only one year to sue the landlord. This is the exact language in the lease:

Limitation on Actions. To the extent allowed by law, Resident also agrees and understands that any legal action against Management or Owner must be instituted within one year of the date any claim or cause of action arises and that any action filed after one year from such date shall be time barred as a matter of law.

Focusing on the word any, the Court of Appeals ruled that any legal action included not only breach of contract claims but also personal injury claims. Thus, the lease trumped Georgia’s statute of limitations. The Court reasoned that parties should be free to enter into contracts without interference from the courts.

At Gomez & Golomb, we practice personal injury and real estate litigation. Thus, for us, Langley cuts both ways. It’s bad for our personal injury clients, but good for our real estate and corporate clients. From now on, in personal injury cases, we will be looking even more closely at applicable contracts for language that may limit injury claims. For our real estate and corporate clients, we will be advising them that Langley opens the door to include terms in their contracts that limit liability.

Bankruptcy: repeat filings

A question we get frequently, especially after a debtor files a second or third bankruptcy as a delay strategy, is just how many times can a debtor get away with filing for bankruptcy? We refer to these folks, not so affectionately, as “serial filers.” While not perfect, there are some restrictions for debtors filing multiple bankruptcies:

180 days: A debtor can’t file a second bankruptcy case for 180 days if the debtor’s case was dismissed (i.e., the bankruptcy wasn’t completed) for the following reasons: (1) by the court for willful failure of the debtor to abide by orders of the court, or to appear before the court in proper prosecution of the case; or (2) the debtor requested and obtained the voluntary dismissal of the case following the filing of a request for relief from the automatic stay.

Two bankruptcies in one year: When a debtor files a second bankruptcy within one year of the dismissal of the first case, the automatic stay expires 30 days after filing (11 U.S.C. § 362(c)(3)). There’s one exception, which is if the debtor can prove to the court that the second case was filed in good faith (meaning the debtor didn’t file repeatedly to delay collection by a creditor), the court has discretion to extend the automatic stay.

Three bankruptcies in one year: When a debtor files a third bankruptcy within one year of the dismissal of the first case, the automatic stay doesn’t take effect at all upon the third filing (11 U.S.C. § 362(c)(4)).

After successful completion of a bankruptcy (i.e., a discharge): For a Chapter 7 bankruptcy, a debtor is not eligible for a discharge if the debtor received a discharge in another Chapter 7 filed within the prior eight years, or in a Chapter 13 case filed in the prior six years (unless the prior Chapter 13 payment plan either paid 100% of the unsecured claims or paid 70% of the unsecured claims). For a Chapter 13 bankruptcy, a debtor is not eligible for a discharge if the debtor received a discharge in another Chapter 13 case filed in the prior two years, or in a Chapter 7 case filed in the prior four years.

Miscellaneous note: The one-year period for either termination or non-application of the stay begins to run from the date of dismissal of the first case. In a joint case, if only one of the debtors had a prior case dismissed in the year before filing, the automatic stay is affected only as to the debtor with the prior case. Section 362(c) (3) and (4) apply to the acts of a specific debtor rather than joint debtors in the aggregate.

Please call us if you need clarification or have any questions.

Attorney’s Fees in Georgia: Part One

Part 1: Contractual Attorney’s Fees

Virtually without fail, one of the first things our clients ask is whether they’ll be able to recover attorney’s fees from the other side. This is a fair question because it seems wrong to have pay an attorney when the other side has acted improperly or has caused the dispute. While not necessarily intuitive, the default rule, with exceptions, is that each side is responsible for their own attorney’s fees. We’re going to discuss some of the statutes and cases contrary to the default rule–these laws allow the winner of a lawsuit to recover reasonable attorney’s fees.

The most clear cut situation in which the winning party can recover attorney’s fees is when parties have signed a contract that provides for the recovery of attorney’s fees. For example, a typical provision in a contract might say that “the prevailing party is entitled to attorney’s fees incurred to enforce or collect monies due under the contract.” In these situations, a trial court doesn’t have the authority to alter such an arrangement unless it is prohibited by statute, and the winning party is entitled to reasonable attorney’s fees as a matter of law.

Contractual attorney’s fees were discussed by the Georgia Court of Appeals in Summit At Scarborough Homeowners Association, Inc. v. Williams, A17A1289 (decided November, 16, 2017). In that case, the trial court’s decision to deny a homeowner’s association attorney’s fees related to unpaid association dues was reversed because the association documents, which are considered a contract, provided for the collection of attorney’s fees. Thus, in cases where a contract provides for attorney’s fees, the trial court must award attorney’s fees based upon evidence of the reasonable value of the professional services provided by the attorney.

In the next installment, we’ll discuss what happens when there’s no contractual provision for attorney’s fees, but the opposing party has acted in bad faith.

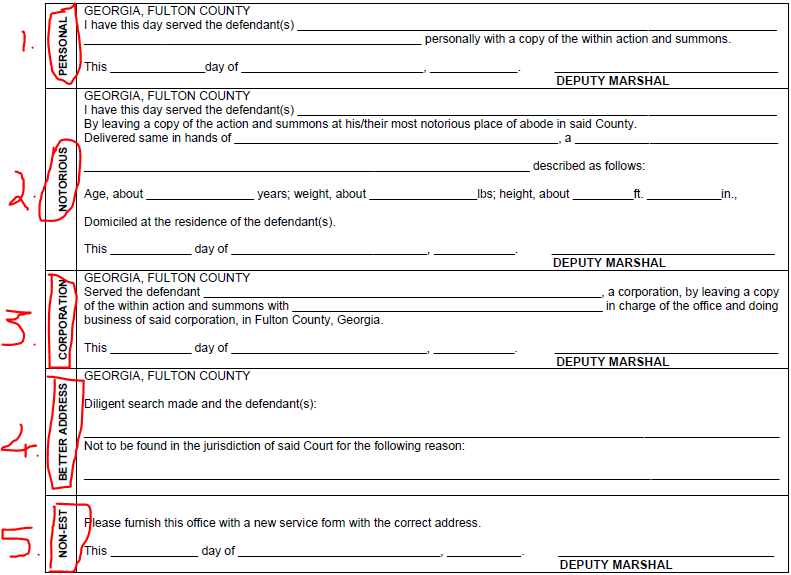

Serving a Lawsuit in Georgia: Understanding the Sheriff’s Entry of Service Form

In Georgia, with some exceptions, the opposing party a/k/a the defendant must be “personally” served before a lawsuit can go forward. This means the lawsuit must be physically handed to the defendant. If the defendant is a corporation, service is made on the corporation’s registered agent. (Every corporation in Georgia is required to appoint a registered agent—this information can be found on the Georgia Secretary of State’s website.)

Service usually begins by providing the sheriff a copy of the complaint, summons, and sheriff’s entry of service form. Service by the sheriff typically takes two to three weeks, during which time a sheriff’s deputy will complete the form and mail it back to the filing party. What does this form mean? Below is the relevant part of the form and how we address the various types of service in our office:

If the “personal” box is completed (box # 1 above), almost always, the sheriff has handed the paperwork to the opposing party and service is complete. Now we can get to work on the case.

If the “notorious” box is checked (box # 2 above) this means the sheriff has handed the paperwork to someone over 18 years old who lives the opposing party. Georgia law allows notorious service, but, in our experience, we should be cautious in these situations because notorious service is sometimes unreliable and can challenged. Fortunately, an answer is due from the opposing party 30 days after service. If service isn’t contested in the answer, we no longer need to worry about service. If service is contested in the answer and seems reasonable, we will discuss with you the merits of repeating service. Ultimately, getting proper service is important because if we don’t have proper service, any judgment we obtain might be overturned.

The “corporation” box (box # 3 above) obviously applies to serving a corporation. If this is checked, generally, this ends up being successful service.

If the “better address” box is checked (box # 5 above) this means the person living at the address provided has told the sheriff that opposing party has moved.

Finally, the dreaded “non-est” box box # 5 above): this means the sheriff has gone to the address provided but was unable to serve the defendant. Most importantly, this means the lawsuit can’t continue. At this point, we need to determine if we have a good address for the opposing party. A defendant can be served at home, work, church, etc. If we are confident we have a good address despite the sheriff being unsuccessful, we recommend hiring a private process server. Unlike the sheriff, a private process server will work with us and has a much better chance of successfully serving the defendant. The cost for a private process server is about $100, but goes up depending on difficulty. If we aren’t confident that we have a good address, we recommend hiring an investigator to find a good address for the defendant. This is more expensive and will cost $250 and upwards.

If we still can’t find the defendant or believe the defendant is avoiding service, we’re entitled to ask the court to allow us to serve the opposing party by publication. We’ll address service by publication in a separate blog.

We hope this gives you a better idea regarding service of a lawsuit in Georgia. If you have any questions, please don’t hesitate to call us at 404-382-9994.